RaPID© is a state of the art software based on a web interface (Edge, Firefox, Chrome and Safar) and an Oracle database covering risk, accounting, controlling, regulatory reporting and treasury for financial institutions. The current facts sheet describes only IFRS 9, IFRS 17 and budgeting for insurers only.

Workflow

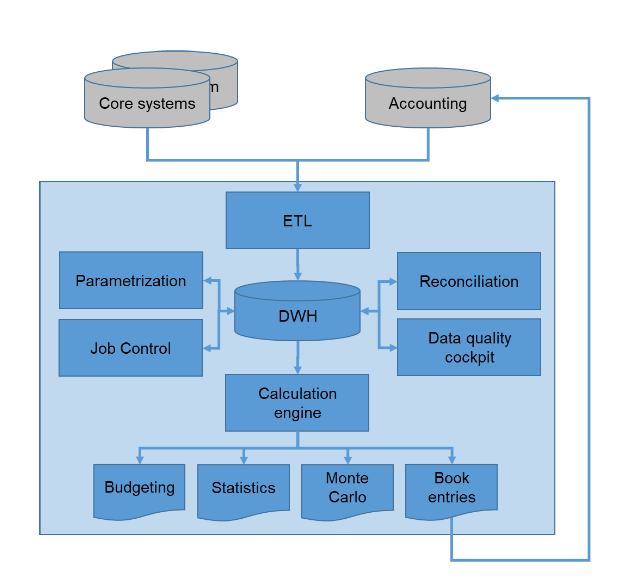

RaPID has a fully integrated ETL (extract / transform / load) that allows to interface any core system and map all assets and liabilities. A data quality cockpit measures and amends the data. All data is historized in an Oracle DWH. All processes can be automated. Results are either shown in internal reports or book entries are written back to the accounting system

IFRS 9

- Constant effective yield

- Amortized cost

- Fair value

- Expected credit loss (ECL)

IFRS 17

- Covered policy types: life, PC, health, pension and reinsurance.

- Level of aggregation / portfolio

- Measurement at initial recognition

- Subsequent measurement

- General measurement model (GMM)

- Fulfillment cash flow

- Combined ratio, insurance risk / risk adjustment

- Contractual service margin (CSM)

- Life, non-life, reinsurance, health, pension with stochastic cash flow modeling based on various frequency and severity distributions: Poison, geometric, log series, negative binomial, beta binomial, exponential, pareto, Weibull, Gamma, normal, half normal, and uniform.

RaPID is powerful, easy-to-use and a comprehensive Management Information System (MIS) including:

- Drill downs / up to a single contract

- slicing & dicing according

- Onerous contracts

- Variable Fee approach (VFA)

- Premium allocation approach (PAA)

- Investment contracts with a DPF

- Insurance service result

- Insurance finance income & expense

- Derecognition

- Local GAAP versus IFRS 17

- Generation of the monthly book entries for the general ledger

Other risks

Liquidity risk:

- Liquidity risk: gap analysis (marginal, cumulative, and residual), liquidity ratios (liquid / assets, illiquid assets / assets, loan to deposit ratio), funding, management

Credit risk

- Exposure analysis according to various dimensions, with / without collateral and guarantees.

concentration risk and large exposure analysis with respect to customers, currencies, countries / geography, sectors, etc. - Stress testing of ratings, probabilities of default, recovery rates

Expected credit loss (ECL)

Market risk

- Net present value, duration, convexity, yield-to-maturity, option Greeks

- Stress testing of various risk factors

- Stress testing of various risk factors

- ALM / interest rate risk / Sensitivity analysis

Cash flow engine

Sophisticated cash flow engine covering all asset, liabilities, derivatives, and off-balance contracts like

- Loans, mortgages, step-up / down, roller coaster, fixed deposits, issuances, non-maturity account

- Interest rate swaps, swaptions, futures, options

- Basket, private equity, commodities

- more than 150 pre-defined reports

- BI report generator

Budgeting local GAAP, IFRS and US GAAP

- Parallel calculation of local GAAP, IFRS and US GAAP

- What-if analysis

- Book engine

- RAROC, RORAC, RARORAC

- Time series analysis

- Performance analysis

- Monte Carlo simulation

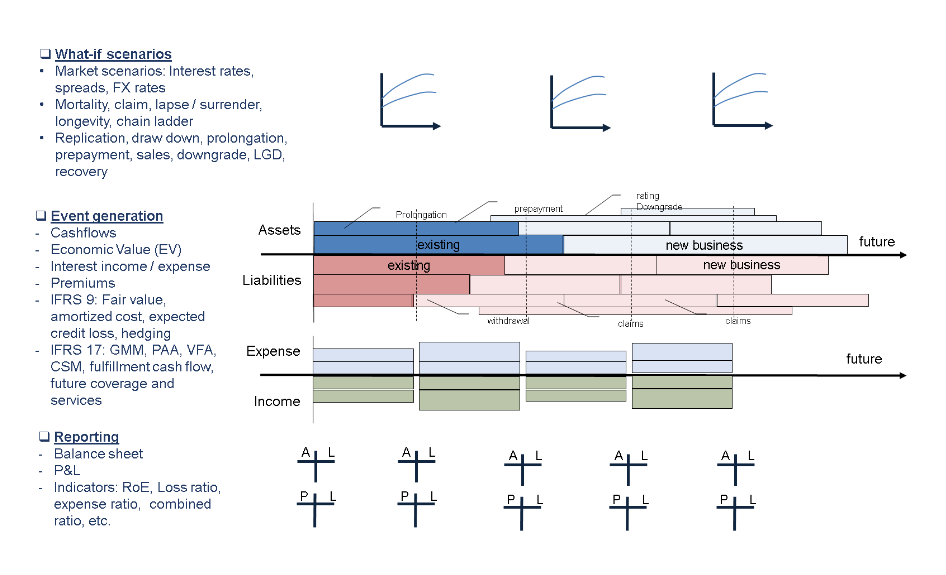

The following chart shows the overview of the forecasting / budgeting for the whole balance sheet under several scenarios and assumptions. The analysis can be based on what-if or Monte Carlo scenarios.